comparison

Level vs. Graded vs. Guaranteed Issue: Which Fits Your Health?

Compare level, graded, and guaranteed issue burial insurance side by side: immediate vs. delayed benefits, cost differences, and which fits your health.

Updated June 25, 2026 · 7 min read

We see the stress families face when trying to figure out how to cover final expenses.

According to the National Funeral Directors Association in 2026, a traditional funeral with a viewing and burial now carries a median cost of $8,300. This data point is exactly why having the right coverage matters so much.

Our team at Nationwide Final Expense was founded with a simple mission: to provide exceptional final expense life insurance services that customers can truly rely on. Picking the wrong plan can leave your loved ones with unexpected bills.

Comparing level vs graded vs guaranteed issue policies is the most important step in securing your final arrangements.

We want to walk you through the data behind these three options, explain how they actually work, and outline exactly how to pick the right one for your health profile. Understanding these differences will save you money.

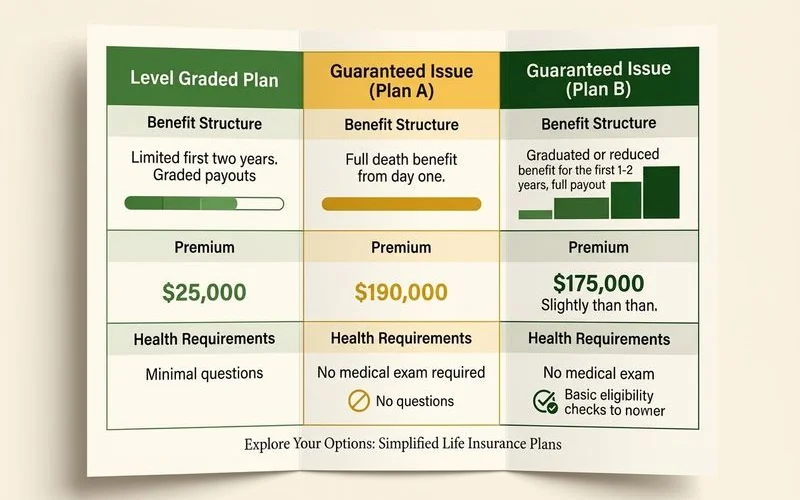

The three tiers, at a glance

Burial insurance is typically sold in three tiers based entirely on your current health profile and how quickly the death benefit pays out. These tiers are level, graded, and guaranteed issue whole life coverage.

We often explain that your medical history dictates which tier you qualify for. Choice Mutual’s 2026 pricing analysis shows that seniors typically pay an average of $50 to $100 per month for a $10,000 policy. The exact price you pay depends heavily on which of these three tiers a carrier places you in.

- Level (immediate full benefit). Full death benefit is in force from day one. This tier offers the cheapest premium per dollar of coverage. It requires answering “no” to most serious-condition questions on the application.

- Graded (stepped benefit). A partial benefit pays out in year one, a larger partial benefit pays out in year two, and the full benefit begins from year three onward. Premium costs run slightly higher than a level plan. This option accepts applicants with managed serious conditions or an older heart and stroke history.

- Guaranteed issue (modified benefit). The carrier provides a premium-plus-interest refund if death occurs in years one or two, and sometimes year three depending on the plan. Full benefits begin after this waiting period ends. This tier carries the highest premium of the three choices. It accepts virtually all applicants, as it is built specifically for adults declined elsewhere.

Our agency sees the same Funeral Advantage product sold across all three of these tiers. The main difference is which tier you qualify for, rather than which product you bought. See Guaranteed Acceptance Burial Insurance for the overall product details.

Level coverage in detail

Level coverage provides a fixed premium and an immediate, full death benefit from the day your policy is issued. This means the carrier pays the entire face amount to your beneficiary whether you pass away tomorrow or in 30 years. The cash benefit pays out within 24 hours of claim approval.

We consider this the gold standard for relatively healthy applicants. Many seniors mistakenly assume they will not qualify for a level death benefit because of minor health issues. The CDC reports in 2026 that nearly 119 million adults in the US have high blood pressure, yet this does not automatically disqualify you.

Our underwriting experience shows that well-managed conditions are perfectly acceptable. Common conditions that still qualify for level coverage include:

- Controlled high blood pressure

- Controlled diabetes without insulin issues

- Arthritis and cholesterol management

- Mild COPD or a history of skin cancer

Recent health events carry much stricter penalties. A recent heart attack or stroke within the last 12 months will disqualify you from this tier. Recent active cancer, advanced COPD, congestive heart failure, dementia, and hospice care also prevent approval.

We recommend applying early to secure the lowest possible rates. MoneyGeek’s 2026 rate analysis reveals that a healthy 50-year-old woman might pay just $30 per month for $10,000 in level coverage. Age plays a massive role in pricing, so locking in your premium now provides long-term financial relief.

Graded coverage in detail

A graded death benefit is a middle-tier feature where the payout increases over the first few years. Typically, a policy pays 30% in year one, 70% in year two, and the full 100% from year three onward, though exact percentages vary by carrier.

We find that this structure perfectly bridges the gap for individuals with managed serious conditions. Premium costs run slightly higher than level coverage. A 2026 market review shows these policies generally cost 15% to 30% more for the exact same face amount.

Our carrier partners price it this way because they accept a significantly higher risk. Applicants who fit perfectly into this category usually have:

- A heart attack or stroke history older than two years

- Moderate COPD

- Diabetes with some complications

- Cancer in remission for two to five years

We always point out the value of having at least partial protection immediately. The graded structure provides meaningful cash during the first two years rather than zero. This ensures your family has some financial support while still letting the carrier accept higher-risk applicants.

Why not just buy graded if level is available?

Premium costs are the deciding factor. Level is cheaper for the exact same face amount. If your health profile qualifies you for level coverage, you should absolutely take it.

Guaranteed issue (modified benefit) in detail

Guaranteed issue whole life is a policy tier where no one is declined, built entirely on a modified benefit structure. If you pass away within the waiting period of two to three years depending on the plan, your beneficiary receives all premiums paid plus interest. This interest rate typically sits at around 10%.

We know this product is a lifeline for applicants with severe or recent medical histories. If you survive past the waiting period, the full death benefit goes into force. Accidental death is usually covered in full from day one regardless of the waiting period.

Our team encourages you to review the specifics of this timeline. For deeper detail on how the structure actually works, see how the waiting period works.

This tier was designed specifically for anyone declined by the level and graded categories. It readily accepts applicants dealing with:

- Serious recent diagnoses

- Advanced COPD or congestive heart failure

- Dementia

- Recent cancer treatments

We caution clients that this tier carries the highest monthly cost. For a 70-year-old buying $15,000 of coverage, guaranteed issue might be 30% to 50% more per month than a level plan.

Carrier data from 2026 shows that companies like Gerber Life and Great Western specialize in these guaranteed approvals. The steep price trade-off is often necessary because it is the only coverage that will accept the applicant.

How to pick

Your current medical history and age dictate the right plan for your needs. Apply with full honesty about your current condition.

We handle the heavy lifting of matching your profile to the correct tier. The advisor or the underwriting decision on the application places you in the right category. Your job is to simply complete three steps:

- Confirm your required coverage amount

- Select the most generous immediate benefit structure

- Accept the premium rate that fits your budget

Our advisors recommend prioritizing immediate benefits whenever possible. If you have a choice between two tiers, choose the one with the highest day-one coverage.

For example, you might qualify for graded coverage but the application also offers you a level plan at a slightly higher premium because of one specific factor. Taking the level plan in that scenario is always the smarter financial move.

We work with over 30 A-rated insurance carriers to scan the US market for your best option. To find out which tier you would qualify for, call (800) 930-7459.

The conversation takes about 10 minutes. Most callers get a decision the exact same day.

Frequently Asked Questions

Which plan tier is cheapest?

Can I switch tiers after I buy?

Is graded the same as guaranteed issue?

Learn more about Guaranteed Acceptance Burial Insurance

Whole life burial coverage with no medical exam and easy qualification, built for seniors with health concerns or prior denials.

Explore Guaranteed AcceptanceRelated Guides

Burial Insurance After Being Denied Life Insurance

Been declined for life insurance? Guaranteed acceptance burial insurance is built for you — no exam, pre-existing conditions accepted, here's what changes.

Burial Insurance With No Medical Exam, Explained

No-medical-exam burial insurance uses a one-page application. Learn how simplified-issue works, the health questions, and who qualifies same-day.

Can You Get Burial Insurance With Pre-Existing Conditions?

Yes — most applicants with pre-existing conditions can get burial insurance. Which conditions are accepted, the health questions, and the no-exam process.

Guaranteed Acceptance vs. Simplified Issue Burial Insurance

Compare guaranteed acceptance and simplified issue burial insurance: underwriting, premiums, and waiting periods — and which fits your health profile.