Have you ever worried about how a sudden medical need might affect your life savings?

We hear this concern every single day at Nationwide Final Expense.

Texas Medicaid limits countable assets for an individual to just $2,000. That strict limit often stands between seniors and the long-term care they need. We want to help you protect your final arrangements without violating those rules.

Irrevocable funeral trusts are legally binding agreements used in Central Texas planning conversations. Properly structured, these trusts hold a final expense policy and make the cash value an exempt asset under Texas regulations.

We will show you exactly how this strategy keeps your countable assets under the threshold.

Your final expenses stay covered.

This approach makes sense if you anticipate Medicaid being part of your future care plan. We invite you to explore how to secure your burial expenses without relying on family contributions or county aid.

Why the Texas $2,000 asset limit matters

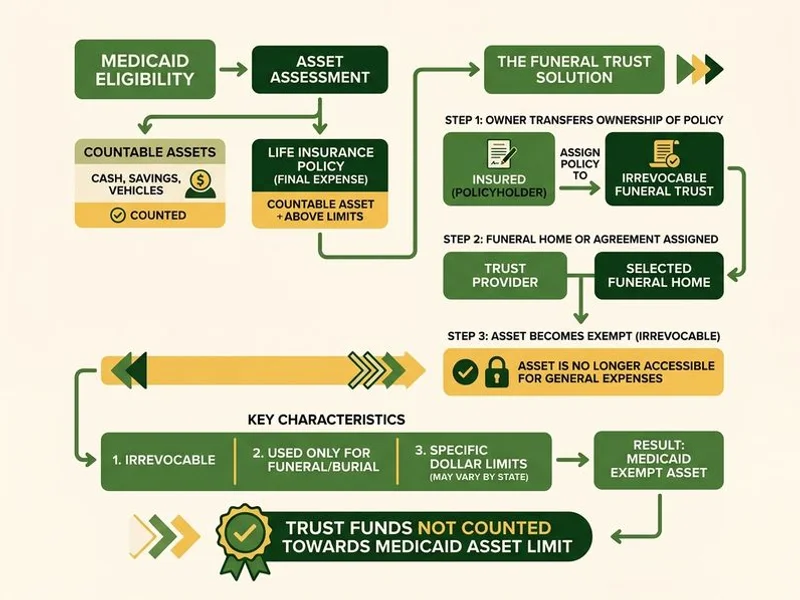

Texas Medicaid evaluates countable assets when determining eligibility. These assets include bank accounts, brokerage holdings, and the cash surrender value of certain insurance policies. We know the cost of care can drain these accounts incredibly fast. In 2026, the average cost of a semi-private room in a Texas nursing home exceeds $6,500 per month.

If you exceed the $2,000 limit, the state typically requires you to spend down your money to qualify for aid. Spending down on funeral costs in advance provides a smart way to reduce your countable assets. We often see financial planners use this strategy to fund exact burial costs. An irrevocable funeral trust serves as the legal vehicle that holds that earmarked money.

The irrevocable nature of the trust is the most important feature. Because you cannot pull the funds back, Texas Medicaid stops counting them against your asset limit. We understand that giving up control sounds intimidating at first. You give up access to the cash value, and the state grants you the asset exemption in return.

Countable vs. Exempt Assets

| Asset Type | Medicaid Status |

|---|---|

| Checking and Savings Accounts | Countable (Subject to $2,000 limit) |

| Standard Life Insurance Cash Value | Countable |

| Irrevocable Funeral Trust Funds | Exempt |

How irrevocable funeral trusts fit with a final expense policy

This trust does not replace your underlying guaranteed acceptance burial insurance, but rather serves as a protective container for it. We guide families through a very straightforward flow. A Funeral Advantage whole life policy is purchased first. The legal document is then drafted under Texas Health and Safety Code Chapter 697.

This specific chapter governs prepaid funeral benefits across the state. We highly recommend working with a Texas-licensed elder law or estate planning attorney for this legal step. Ownership of the policy legally transfers directly to the trust.

At the time of need, the death benefit pays out for funeral expenses through the trust. Your family still gets the fast 24-hour claim payout that a Funeral Advantage policy promises. We remind clients that the order of operations matters deeply here. Sequencing the policy purchase and the trust setup correctly prevents a paperwork disaster.

The Correct Setup Sequence

- Calculate your target coverage: The average traditional funeral in Texas costs around $8,700 in 2026, while direct cremation averages $1,995.

- Purchase the policy: Secure a final expense life insurance plan to fund the exact amount you need.

- Draft the legal trust: Have a qualified attorney prepare the document under Chapter 697.

- Transfer ownership: Assign the policy directly to the irrevocable trust to complete the exemption process.

When this planning combination makes sense

This specific combination works best if you or a parent are planning for the possibility of needing nursing home care covered by Texas Medicaid. We look at the statistics to understand the real risks. Recent data shows that roughly 70% of adults turning 65 will require some form of long-term care during their lifetime. About 20% of those individuals will need care for more than five years.

You want your burial expenses covered in advance so your family does not have to scramble for funds. You must also be willing to give up access to the money in the policy.

The defining rule of an exempt asset is simple: you must surrender control of the funds to guarantee your Medicaid qualification and protect your family’s financial future.

We emphasize that this strategy does not make sense for everyone. If you do not expect Medicaid to be part of your situation, a standalone final expense policy is usually enough without the need for irrevocable funeral trusts.

If you want to talk through whether this combination fits your life, please call (800) 930-7459. We have licensed advisors ready to explain how the sequencing works. A professional can also point you to a Texas-licensed attorney for the necessary trust paperwork. There is absolutely no obligation, and the call is completely free.

Medicaid planning across Central Texas

We help seniors and their adult children plan asset protection throughout the region, including Austin, Round Rock, and Hutto. For families coordinating Medicaid eligibility with county programs, we also explain how Travis County burial assistance, Williamson County burial assistance, and Hays County burial assistance interact with a funeral trust.