process

How to Protect Burial Funds From Medicaid Spend-Down in Texas

How an irrevocable funeral trust shelters burial funds from Texas Medicaid spend-down by converting cash value into an exempt asset — step by step.

Updated June 25, 2026 · 7 min read

We see families struggle with strict state regulations every single day. Qualifying for Texas long-term care Medicaid requires an individual to keep countable assets strictly under $2,000. This extremely low threshold catches many seniors off guard when they suddenly need nursing home care.

Our goal is to help you manage this transition smoothly.

The existing balance in checking accounts and other savings will easily push applicants over the limit. “Spend-down” is the process of legally reducing those countable assets to the qualifying level. The main challenge is handling this spend-down in ways that actually benefit your family.

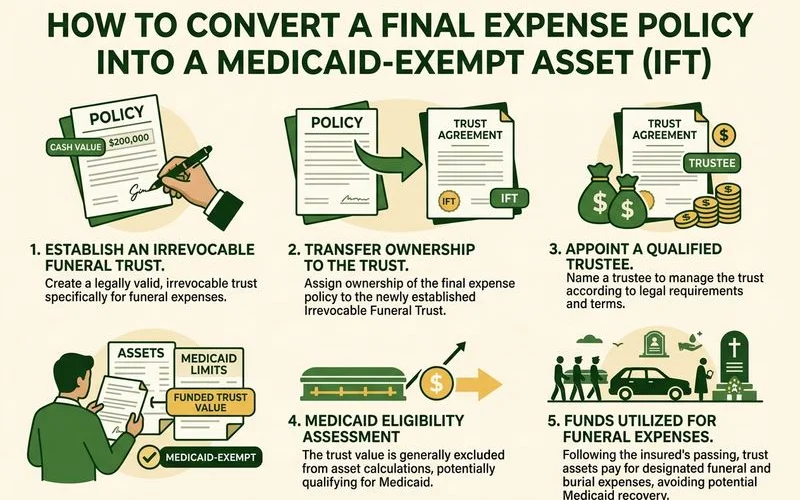

We rely on an irrevocable funeral trust because it is the specific legal vehicle that makes this financial structure work. Prepaying for a funeral is one of the standard categories the Texas Health and Human Services Commission (HHSC) allows as an exempt purchase. The visual guide below shows exactly how this conversion functions.

The spend-down problem

We frequently help clients who face immediate disqualification over a basic checking account balance. The core problem is that excess funds must be spent before the state will pay for long-term care. Finding ways to spend this money productively is difficult under immense time pressure.

We want you to be aware of the 2026 Texas financial limits that dictate this entire process:

- Countable Asset Limit: $2,000 for a single applicant.

- Income Cap: $2,982 per month for nursing home care.

- Home Equity Limit: Up to $752,000 is generally exempt.

Our advisors recommend using a specific portion of your excess funds to secure your final arrangements. The state approves this exemption only when you follow their strict procedural rules. Failing to adhere to the HHSC guidelines will result in a penalized, non-exempt asset transfer.

How the structure works

We design this process to legally convert a countable cash asset into an exempt funeral policy. The structure requires buying a final expense policy, drafting an irrevocable trust, transferring ownership, and securing casework approval. This proven strategy safely shelters your money from Medicaid calculations.

Our step-by-step guide walks you through exactly how to set this up.

Step 1: Buy a final expense policy. You need to purchase a policy with a $10,000 to $15,000 face amount. The exact size depends heavily on your chosen final arrangements. We frequently utilize a Funeral Advantage whole life policy or similar product for this requirement. In 2026, a traditional burial in Texas averages around $8,800. Direct cremation costs are much lower at about $2,135.

Step 2: Draft an irrevocable funeral trust. Our clients must complete this crucial legal step with a Texas-licensed elder-law or estate-planning attorney. The trust document explicitly names the trust as the owner of the policy. Legal paperwork must specify that these funds are exclusively for funeral and burial expenses.

Step 3: Transfer ownership of the policy to the trust. We consider this ownership transfer the most critical point in the entire process. You must complete this transfer correctly to trigger the Medicaid exemption. The trust itself must legally own the policy, rather than just being listed as the beneficiary.

Step 4: Confirm the structure with the Medicaid caseworker. We help families document that the irrevocable trust owns the policy during the Medicaid application. This documentation proves to the state that the policy is no longer a countable asset. The final result is that the cash value of the policy is now a fully exempt asset under Texas Medicaid rules.

Our clients feel immense relief knowing the strict $2,000 individual asset limit no longer applies to that specific money.

The table below outlines how different choices impact your required policy size:

| Funeral Type in Texas (2026 Data) | Average Estimated Cost | Recommended Policy Size |

|---|---|---|

| Direct Cremation | $2,135 | $3,000 - $5,000 |

| Affordable Green Burial | $5,262 | $6,000 - $8,000 |

| Traditional Full-Service Burial | $8,800+ | $10,000 - $15,000 |

Why “irrevocable” matters

We must emphasize that the Medicaid exemption entirely depends on you completely giving up access to the funds. The legal definition of “irrevocable” means you have permanently surrendered control over the money. A revocable trust does not provide this protection, so the state still considers those funds as available cash.

Our advisors see people mistakenly try to retain access to the cash value. You absolutely cannot cash the policy in, change the beneficiary, or borrow against it. If you retained the power to do any of those things, Medicaid would count the total value toward your $2,000 limit.

We want you to know that a standard life insurance policy outside of a trust only receives a strict $1,500 face-value exemption in Texas.

This arrangement is a necessary trade-off required by state law. You receive the valuable asset exemption in exchange for a permanent loss of financial access. Our clients typically find this trade highly worthwhile when they have $5,000 to $15,000 sitting in a checking account designated for burial costs.

For the underlying asset-limit detail, see Texas $2,000 Medicaid asset limit.

The 60-month look-back period

Texas Medicaid long-term care has a 60-month look-back period for asset transfers. Transferring assets within that window (other than to certain exempt categories like a funeral trust) can trigger penalty periods. Funeral trusts are an exempt category, but the structure has to be done correctly. Work with an elder-law attorney to ensure timing and structure satisfy the rules.

Avoiding Common Trust Mistakes

We strongly advise reviewing the specific limits before funding your trust. Texas caps the amount you can place into an irrevocable burial contract at $15,000 per applicant. Funding the trust beyond this state-mandated limit is a frequent error that forces a stressful, last-minute asset spend-down.

Our experience shows that keeping the policy face value strictly aligned with a realistic Goods and Services Statement prevents application delays. Doing so ensures the HHSC caseworker can quickly approve your paperwork without questioning the amounts.

The team you need

We believe this is one specific situation where you genuinely require professional help across three distinct roles. Attempting this complex legal and financial maneuver on your own usually results in costly errors. The structure requires tight coordination between legal, insurance, and state professionals.

Our founders started Nationwide Final Expense with a simple mission: to provide exceptional final expense life insurance services that customers can truly rely on. That deep experience means acknowledging when outside experts are mandatory to protect your eligibility. You need the following professionals to execute this plan correctly:

- Elder-law or estate-planning attorney: This expert drafts the trust paperwork in strict compliance with Texas Medicaid rules. A properly drafted document is the only way the state will classify the trust as exempt.

- Licensed life insurance agent: This professional issues the final expense policy that the newly created trust will hold. We handle this side of the process every day to ensure exact compliance.

- Medicaid caseworker (or planner): This state employee or private consultant confirms the entire structure satisfies the eligibility requirements for your specific case.

We urge you to coordinate these three roles in a very precise order. The insurance policy goes in first, followed by the trust draft, the ownership transfer, and finally the Medicaid application submission. Applications can stall for months because families completed these steps out of sequence or submitted incomplete paperwork.

What if you’re already in spend-down

We frequently help families who are currently spending down assets to meet an urgent Texas Medicaid deadline. You can absolutely still set up a funeral trust while actively spending down. The precise timing just becomes much more critical to avoid violating the 60-month look-back period.

Our team suggests that a local elder-law attorney should be your very first phone call in this scenario. The attorney can accurately confirm what timeline works for your specific financial situation. They will ensure your purchase is officially categorized as an exempt expense rather than an improper gift.

We can easily coordinate the insurance side of the equation once the legal strategy is approved. Securing this protection takes less time than most people expect.

If you need help finding a Texas-licensed elder-law attorney and pricing the underlying final expense policy, call (800) 930-7459. Our licensed agents can quote the policy in about 10 minutes and point you toward qualified legal professionals in the Austin area. Take action today to protect your hard-earned savings while ensuring your final wishes are honored.

Frequently Asked Questions

What is the Medicaid spend-down rule in Texas?

Is an irrevocable funeral trust the same as a preneed contract?

When should I set up a funeral trust?

Learn more about Irrevocable Funeral Trusts

How Central Texas seniors can shelter burial funds from Medicaid spend-down while keeping final expense coverage.

Explore Funeral TrustsRelated Guides

Irrevocable Funeral Trust vs. Final Expense Policy

Do you need a funeral trust, a final expense policy, or both? Compare the Medicaid-planning use case with general coverage, control, and how they combine.

The Texas $2,000 Medicaid Asset Limit and Funeral Trusts

Texas Medicaid caps countable assets at $2,000 for an individual. See what counts, who needs to plan, and how a funeral trust protects burial funds.