qualifier

The Texas $2,000 Medicaid Asset Limit and Funeral Trusts

Texas Medicaid caps countable assets at $2,000 for an individual. See what counts, who needs to plan, and how a funeral trust protects burial funds.

Updated June 25, 2026 · 6 min read

We frequently see Texas families completely caught off guard by the strict financial rules for long-term care.

You likely know that the 2026 income cap of $2,982 per month causes stress, but the severe limits placed on lifetime savings are usually the real dealbreaker. Nationwide Final Expense was founded to provide exceptional final expense life insurance services you can rely on, and our team wants to break down the texas medicaid asset limit funeral rules to show you exactly how to protect your hard-earned money.

Let’s look at the data, what the state actually requires, and how specific tools keep your funds secure.

The number that determines eligibility

To qualify for Texas long-term care Medicaid as an individual, your countable assets must sit under the strict texas medicaid 2000 dollar limit. This figure applies to nursing home coverage and community-based services administered through Texas Health and Human Services.

Our specialists constantly see applicants confused by how this tiny number is calculated. Above the limit means you pay out of pocket, while staying below the limit grants access to essential support.

The state distinguishes sharply between what is countable and what is exempt. We explain the trust vehicle specifically on the Irrevocable Funeral Trusts page, but this guide focuses on the actual asset framework.

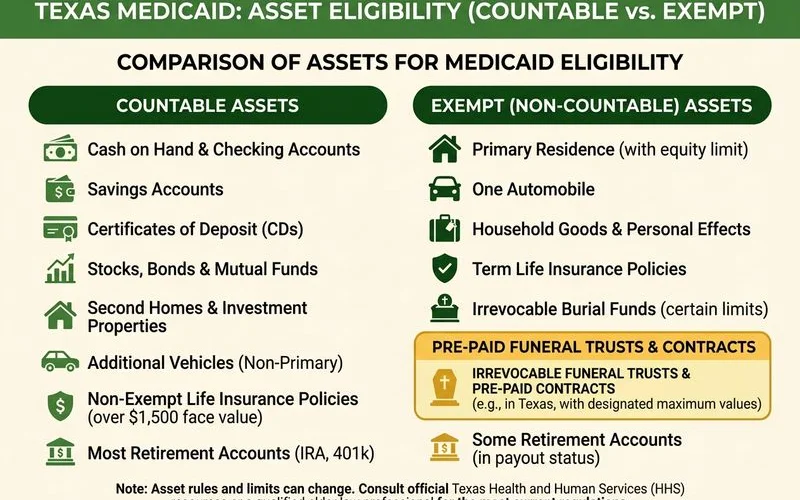

What counts as a countable asset

The general rule dictates that anything you can easily convert to cash for your own use is a countable asset. Our analysts review these rules yearly to keep families informed of the exact requirements. The Texas Integrated Eligibility Redesign System (TIERS) checks financial accounts thoroughly, making full disclosure mandatory.

We categorize these items as the primary countable assets medicaid reviewers target. Specifics include:

- Checking, savings, and money market account balances

- Certificates of deposit, stocks, bonds, and mutual funds

- Cash value of life insurance policies you own personally

- Real estate holdings other than your primary residence

- Extra vehicles, boats, and recreational property

- Cash on hand and most standard IRA balances

Your final expense policy cash value is fully included in this list if you own it directly. Our preferred strategy is using a specialized trust to fix this exact problem.

Avoiding common asset mistakes

Many applicants make critical errors when trying to lower their countable balances. We see people cashing out life insurance policies directly into their checking accounts, which is a major misstep. This action artificially spikes your bank balance and often creates an immediate IRS tax liability.

Another frequent error involves transferring funds to family members. Our recommendation is to always use state-approved spend-down methods instead. Using legitimate tools like a Qualified Income Trust (Miller Trust) handles excess income, but the asset limit requires structural changes.

What’s exempt

Texas exempts primary residences up to a $752,000 equity limit, one vehicle, and specifically structured funeral trusts from the $2,000 calculation. Our goal is to maximize these exact exemptions to protect your wealth. The state allows you to retain certain essential items without penalizing your medicaid eligibility texas status.

We track the annual updates to these exemption thresholds closely. In 2026, the allowable exclusions cover:

- Primary residence (up to a $752,000 equity limit)

- One primary vehicle of any value

- Personal belongings, household goods, and wedding rings

- Burial spaces for the individual and immediate family

- Up to $1,500 in a designated bank burial fund

- Irrevocable funeral trusts holding final expense insurance

- Term life insurance policies with zero cash value

The irrevocable funeral trust line remains the most vital tool for secure burial planning. Our clients use this method to legally shift policy cash value from the countable column to the exempt column. For the step-by-step on how to do this, see protect burial funds from Medicaid spend-down.

The married couple wrinkle

If you are married and your spouse remains at home, Texas allows the “well spouse” to keep substantially more countable assets through the Community Spouse Resource Allowance (CSRA). We closely monitor these federal guidelines because they change annually based on inflation. The standard 2026 CSRA ranges from a $32,532 minimum up to a $162,660 maximum, depending on total marital assets. The community spouse can also retain a monthly income allowance of up to $4,066.50, adding vital nuance to spend-down planning.

How the funeral trust changes the math

The funeral trust legally shifts life insurance cash value from a countable asset to an exempt asset, instantly lowering your final balance. Our team uses a simple comparison to show why this early intervention matters. Without a proper strategy, a senior can easily exceed the strict state limits.

We built this straightforward breakdown to illustrate the difference.

| Asset Category | Without Planning (Countable) | With Funeral Trust (Exempt) |

|---|---|---|

| Checking Account | $14,000 | $14,000 |

| Whole Life Policy Cash Value | $12,000 | $0 (Moved to Trust) |

| Other Miscellaneous Assets | $1,800 | $1,800 |

| Total Countable Assets | $27,800 | $15,800 |

| Amount Over Limit | $25,800 | $13,800 |

Closing the remaining gap

Moving the policy into the trust eliminates a massive portion of the excess funds. Our advisors note that the senior still needs to spend down another $13,800 in this scenario. You can handle this remaining balance through other Texas Health and Human Services approved exempt purchases.

We regularly see families effectively reduce their remaining balances by paying down existing debt or funding home repairs. Other approved methods include maxing out the $1,500 burial fund allowance or prepaying a year of property taxes. The trust acts as the critical foundation piece that makes reaching that final $2,000 goal entirely possible.

When to start planning

You should finalize your asset protection strategy at least 60 months before applying to avoid the state’s five-year look-back penalties. Our experts emphasize that early preparation is the smartest approach to securing your finances. Any unapproved movement of money within that five-year window triggers severe penalty periods.

We want to highlight exactly how these penalties work in 2026. Texas uses a penalty divisor of approximately $262.37 per day to calculate your punishment. Giving away a $10,000 lump sum directly creates a penalty period of roughly 38 days where the state refuses to pay for nursing care.

Properly structured funeral trusts fall into the approved exempt category. Our network of elder law attorneys ensures the paperwork meets exact Texas state requirements to avoid these costly delays.

Immediate needs versus future planning

Families looking five or more years ahead enjoy total flexibility with their asset allocation. We strongly advise taking action early to secure the best possible rates and options. Families facing an imminent facility admission face a highly sensitive timeline requiring precision.

Our support staff is ready to assist with the exact final expense policy the trust requires. Call (800) 930-7459 to get a firm quote in about ten minutes. We can then point you toward qualified Texas elder-law attorneys who handle the specialized trust documentation.

Frequently Asked Questions

Is the limit really only $2,000?

Does my home count?

What about my car?

Learn more about Irrevocable Funeral Trusts

How Central Texas seniors can shelter burial funds from Medicaid spend-down while keeping final expense coverage.

Explore Funeral TrustsRelated Guides

Irrevocable Funeral Trust vs. Final Expense Policy

Do you need a funeral trust, a final expense policy, or both? Compare the Medicaid-planning use case with general coverage, control, and how they combine.

How to Protect Burial Funds From Medicaid Spend-Down in Texas

How an irrevocable funeral trust shelters burial funds from Texas Medicaid spend-down by converting cash value into an exempt asset — step by step.