definition

Burial Insurance With No Medical Exam, Explained

No-medical-exam burial insurance uses a one-page application. Learn how simplified-issue works, the health questions, and who qualifies same-day.

Updated June 25, 2026 · 5 min read

We founded Nationwide Final Expense with a simple mission: to provide exceptional final expense life insurance services that customers can truly rely on. The fear of a doctor’s exam often stops people from securing no medical exam burial insurance. Rising funeral costs make this delay a costly mistake for families.

Our team sees daily how the right information makes the process much less stressful.

Let’s look at the data, what it actually means for your budget, and explore practical ways to respond.

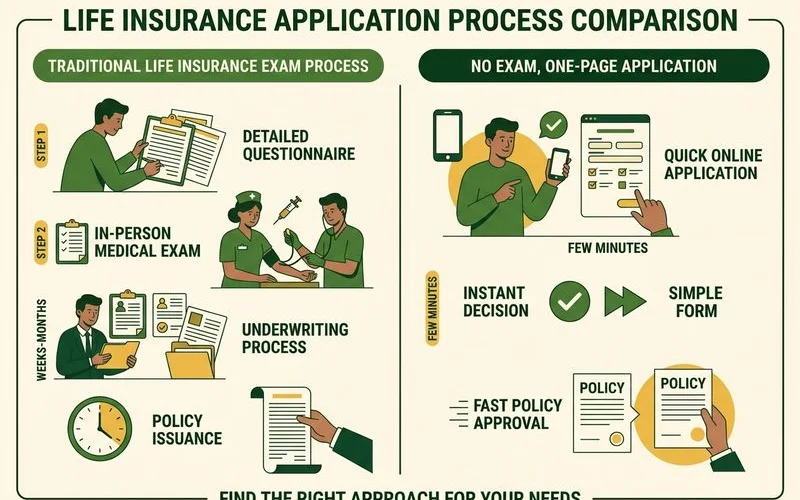

How the no-exam application works

A no medical exam burial insurance application requires only a brief health questionnaire, skipping the usual doctor visits and blood tests. We help clients secure approvals in a single day rather than waiting the typical four to six weeks required for fully underwritten policies. The carrier uses your specific health answers to determine your exact plan tier and monthly rate.

This rapid turnaround is the standard structure for products like Guaranteed Acceptance Burial Insurance and most other final expense policies. Our agency works with top carriers like Mutual of Omaha and Aetna CVS to find you the best fit. These simplified policies remove the stress from securing coverage. Many older adults find this approach much more manageable.

What the application asks

We tell our clients to expect a short questionnaire with about eight to fifteen direct yes or no health questions. The insurance company uses this specific timeline to look for serious medical events within the last twelve to twenty-four months. A clean bill of health on these specific questions usually qualifies you for immediate, level coverage from day one.

Our advisors often see immediate approvals for clients who manage common conditions like high blood pressure or high cholesterol. The application focuses heavily on high-impact conditions, including the following:

- Recent treatment or diagnosis for cancer.

- Heart attacks or strokes occurring in the past 12 months.

- Current use of oxygen equipment for respiratory illnesses.

- A diagnosis of Alzheimer’s, dementia, ALS, or Parkinson’s disease.

- Terminal illness diagnoses with a life expectancy under 12 months.

- Diabetic complications involving amputations or kidney failure.

- Recent major organ transplants.

- Active treatment for substance dependency.

A single “yes” answer usually routes your application to a graded or modified benefit plan. Our team explains this change in real time during the application call to ensure complete transparency. For more on how simplified issue burial insurance and guaranteed-issue tiers differ, see guaranteed acceptance vs. simplified issue. You can use this resource to figure out which option fits your specific applicant profile.

Why the no-exam structure exists

Our data shows that traditional underwriting is designed for younger adults buying massive amounts of coverage. Committing to a half-million dollar policy naturally requires bloodwork and pharmacy checks. This extensive process becomes an expensive and unnecessary overhead for a $15,000 senior whole life policy. We appreciate that the no-exam route keeps administrative costs low and approvals fast. This streamlined setup creates access for folks who would otherwise face an outright decline. The result is a much smoother experience for everyone involved.

What you trade for the simpler application

We always explain that the main trade-off for getting burial insurance without exam is a higher premium per dollar of coverage. A healthy fifty-five-year-old who can easily pass a physical will get more value from a fully underwritten product. The situation changes entirely for applicants over the age of sixty-five with any meaningful health history.

Our experts recommend setting up a clear comparison to understand the value. A simple breakdown helps clarify the exact differences between these options. You will notice how the face amounts and approval speeds vary.

| Feature | Simplified Issue | Guaranteed Issue |

|---|---|---|

| Health Questions | Yes | No |

| Maximum Coverage | Up to $40,000 to $50,000 | Typically capped at $25,000 |

| Approval Speed | Same day to 48 hours | Often same day |

| Waiting Period | None (Day one coverage) | 2 to 3 years (Graded benefit) |

Our representatives note that the guaranteed issue tier is often the only available choice for seniors who have been previously declined. The National Funeral Directors Association reported that the median cost of a funeral with viewing and burial is $8,300 in the US as of 2025. A funeral with cremation averages $6,280, making these smaller policies perfectly sized for actual final expenses rather than massive income replacement.

Our analysis of recent LIMRA data shows the average face amount for a simplified issue policy is $14,535. A guaranteed issue policy averages slightly less at $9,786 per person. These specific coverage amounts directly align with the realistic costs of end-of-life arrangements.

Who this is actually for

We strongly recommend these simplified policies for seniors on fixed incomes who need to cover precise end-of-life costs. The best no exam life insurance seniors can secure usually targets individuals between the ages of fifty and eighty-five. Anyone who has been previously declined for traditional life insurance due to age or medical history should consider this route.

Our clients often choose this path simply to avoid sharing full medical records or scheduling physicals. Fast approvals provide huge relief for families responding to an unexpected, serious diagnosis. An easy phone call can lock in the funds needed to handle the average eight thousand dollar funeral bill.

Our dedicated staff can evaluate your situation and outline the exact tier you qualify for today. You can secure a no medical exam burial insurance policy that brings immediate peace of mind to your loved ones.

Just call (800) 930-7459 to complete the ten-minute application and get your instant decision.

Frequently Asked Questions

How do they decide if I qualify without an exam?

Is no-exam coverage more expensive than exam-based?

How quickly can I get coverage?

Learn more about Guaranteed Acceptance Burial Insurance

Whole life burial coverage with no medical exam and easy qualification, built for seniors with health concerns or prior denials.

Explore Guaranteed AcceptanceRelated Guides

Burial Insurance After Being Denied Life Insurance

Been declined for life insurance? Guaranteed acceptance burial insurance is built for you — no exam, pre-existing conditions accepted, here's what changes.

Can You Get Burial Insurance With Pre-Existing Conditions?

Yes — most applicants with pre-existing conditions can get burial insurance. Which conditions are accepted, the health questions, and the no-exam process.

Guaranteed Acceptance vs. Simplified Issue Burial Insurance

Compare guaranteed acceptance and simplified issue burial insurance: underwriting, premiums, and waiting periods — and which fits your health profile.

How the Modified Benefit Waiting Period Works

Understand the 2–3 year modified benefit waiting period, the premium-plus-interest refund if death occurs during it, and when full benefits begin.