process

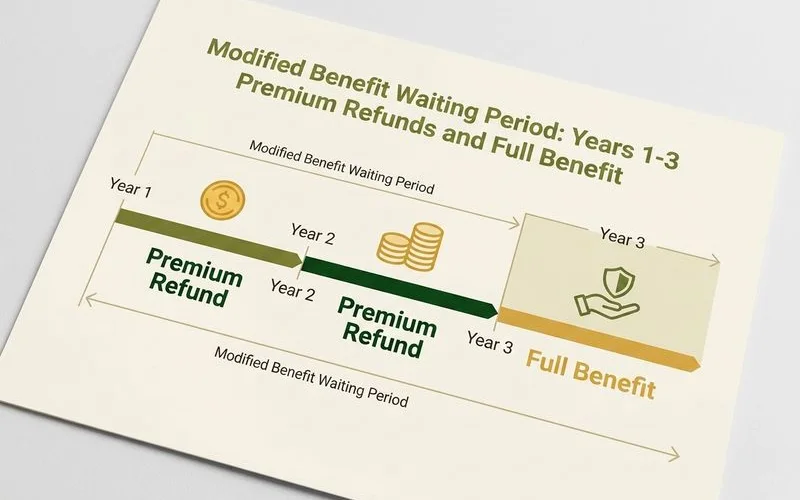

How the Modified Benefit Waiting Period Works

Understand the 2–3 year modified benefit waiting period, the premium-plus-interest refund if death occurs during it, and when full benefits begin.

Updated June 25, 2026 · 5 min read

What the waiting period is, in one paragraph

A modified benefit policy involves a burial insurance waiting period of two to three years before the full death benefit applies. Nationwide Final Expense was founded with a simple mission to provide exceptional final expense life insurance services that customers can truly rely on, especially when understanding these specific terms.

We often hear from clients who feel frustrated after being turned down for standard coverage. If the policyholder passes away from natural causes during that initial window, the policy provides a clear financial return:

- Full Premium Refund: Every dollar paid into the policy is returned to the beneficiary.

- Added Interest: The carrier applies an additional return on top of the premiums.

- Standard Rate: This interest is usually calculated at an annual rate of 10 percent.

Our team knows that this structure exists for one primary reason. It allows carriers to accept applicants who would otherwise face rejection due to severe health history.

This specific design makes the promise of guaranteed acceptance a reality. You can review our Guaranteed Acceptance Burial Insurance guide for the full plan tiers.

Let’s examine how this premium calculation actually works and explore practical ways to secure your family’s financial future.

What “premium plus interest” actually means

“Premium plus interest” means that if the insured dies during the waiting period, the beneficiary receives a full refund of all payments made, along with a set interest rate applied to that total. This calculation ensures that your family never loses the money you invested in the policy.

We want to highlight how competitive this return actually is compared to standard banking products. The national average yield for a basic savings account sits at just 0.61 percent in June 2026.

A modified benefit policy typically calculates your refund with a 10 percent annual interest rate. This significant difference means your money works harder here than it would sitting in a traditional bank account.

Major providers like AIG Corebridge and Gerber Life offer guaranteed issue policies using this exact 10 percent return framework. If you bought a $15,000 modified benefit policy with a $75 monthly premium, your annual cost is $900. Your family is protected from financial loss at every stage.

Let’s break down exactly how this math plays out over time.

| Time of Passing | Premiums Paid | Interest Earned (10% Annual) | Total Beneficiary Payout |

|---|---|---|---|

| Month 8 | $600 | $40 | $640 |

| Month 18 | $1,350 | $135 | $1,485 |

| Month 27 | $2,025 | N/A (Waiting period ends) | $15,000 (Full Death Benefit) |

Our advisors see this structure as a fair compromise for both sides. Carriers can issue coverage to higher-risk applicants without facing immediate large claims.

Applicants secure genuine protection instead of a flat rejection. You can read about how this fits applicants with pre-existing conditions to see who typically utilizes this option.

The accidental death exception

Most modified benefit plans provide full accidental death coverage from the very first day. If you die in a car collision, suffer a fatal fall, or experience any other qualifying accident during the waiting period, the insurance company pays the full $15,000 death benefit. This feature protects against sudden unexpected tragedies that have absolutely nothing to do with your underlying health conditions.

Why this is better than no coverage at all

Securing a modified benefit policy is better than having no coverage because it guarantees your family receives financial assistance. Skipping coverage leaves your loved ones entirely responsible for rapidly rising end-of-life expenses.

We frequently hear from adults who assume a two-year burial insurance waiting period makes the plan worthless. The financial data tells a completely different story. A 65-year-old with congestive heart failure who has been declined for standard coverage faces two distinct choices:

- Option A (Modified Benefit): They purchase a policy for $90 a month. A first-year passing returns all premiums plus 10 percent interest. Surviving past the waiting period activates the full $15,000 death benefit.

- Option B (Skip Coverage): They decline the policy. The family must pay out of pocket for the entire service. The National Funeral Directors Association reports that the median cost of a traditional funeral with a viewing and burial sits at $7,848 as of 2026.

- The Hidden Costs: Cemetery plots, concrete vaults, and headstones are billed separately. These additions often push the total funeral cost well above $10,000.

Our experience shows that a modified benefit serves as a vital financial bridge. It moves families from having absolutely zero options to having guaranteed cash on hand the day the funeral home calls. You should view this plan as a realistic, mathematically sound solution if you have already been rejected by standard carriers.

How to pick the right plan

Picking the right plan requires applying for level or graded coverage first to see if you qualify for immediate benefits. If your health profile rules out those top tiers, a modified benefit plan becomes your most effective path forward.

We always recommend securing level coverage if your application allows it. Premiums are generally lower, and the full death benefit is in force immediately or very quickly.

Modified benefit plans are specifically built for applicants managing severe or chronic health conditions. Common medical situations that typically require a modified benefit include:

- Active treatments for internal cancers

- Recent heart attacks or strokes within the past 12 months

- Congestive heart failure (CHF)

- Severe Chronic Obstructive Pulmonary Disease (COPD)

- Alzheimer’s disease or dementia diagnoses

Our licensed advisors will evaluate your specific medical history to determine exactly which plan you fit.

If a representative places you in a modified benefit tier, you should not view that as a rejection. It is simply the right structural fit for your current health situation.

Please call (800) 930-7459 for a free quote today. We can help you plan for the burial insurance waiting period and confirm which tier applies to you.

Frequently Asked Questions

What happens if I die during the waiting period?

Why does the waiting period exist?

Does the waiting period apply to accidental death?

Learn more about Guaranteed Acceptance Burial Insurance

Whole life burial coverage with no medical exam and easy qualification, built for seniors with health concerns or prior denials.

Explore Guaranteed AcceptanceRelated Guides

Burial Insurance After Being Denied Life Insurance

Been declined for life insurance? Guaranteed acceptance burial insurance is built for you — no exam, pre-existing conditions accepted, here's what changes.

Burial Insurance With No Medical Exam, Explained

No-medical-exam burial insurance uses a one-page application. Learn how simplified-issue works, the health questions, and who qualifies same-day.

Can You Get Burial Insurance With Pre-Existing Conditions?

Yes — most applicants with pre-existing conditions can get burial insurance. Which conditions are accepted, the health questions, and the no-exam process.

Guaranteed Acceptance vs. Simplified Issue Burial Insurance

Compare guaranteed acceptance and simplified issue burial insurance: underwriting, premiums, and waiting periods — and which fits your health profile.