comparison

Guaranteed Acceptance vs. Simplified Issue Burial Insurance

Compare guaranteed acceptance and simplified issue burial insurance: underwriting, premiums, and waiting periods — and which fits your health profile.

Updated June 25, 2026 · 6 min read

We regularly see smart people get tripped up by the fine print in final expense policies. The life insurance industry uses confusing jargon to describe two very different products. You need to know exactly what you are paying for before you sign any paperwork.

Understanding guaranteed acceptance vs simplified issue coverage is the first step.

Our team at Nationwide Final Expense was founded with a simple mission to provide exceptional final expense life insurance services that customers can truly rely on. You deserve to make a confident decision. Let’s look at the data, what it actually tells us, and explore a few practical ways to secure the best policy.

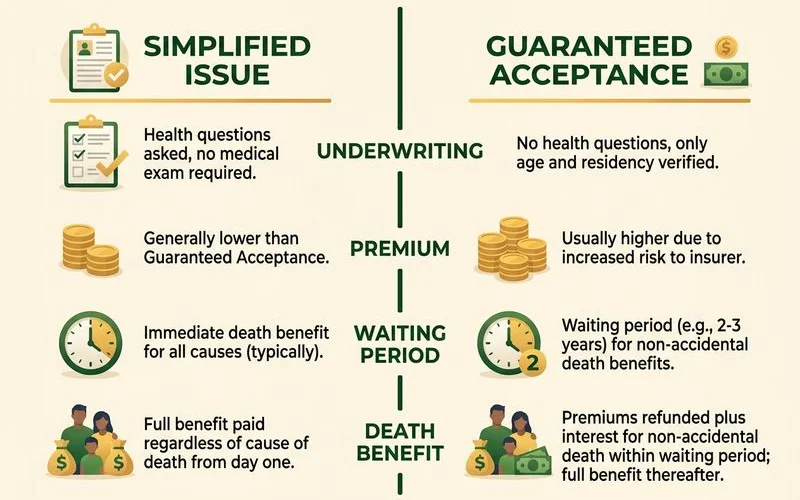

What each one actually means

Simplified issue burial insurance requires you to answer a short medical questionnaire to qualify for immediate coverage. Guaranteed acceptance burial insurance skips the health questions completely but includes a mandatory waiting period before the full death benefit pays out. We know these technical definitions can sound similar at first glance.

Both products live within the broader Guaranteed Acceptance Burial Insurance framework. They share the same carrier and the same Funeral Advantage program, but they use different burial insurance underwriting and pricing for different health profiles. Our agents see the impact of this distinction every day.

Inside Simplified Issue Policies

Simplified issue burial insurance uses a one-page application with 8 to 15 yes or no health questions. There is no medical exam. The carrier evaluates your answers by checking your background to assess risk. They may decline applicants with the most serious conditions.

Premiums stay lower because the carrier successfully screens out the highest-risk cases. You get much more value for your dollar. We see our healthy clients save significant money by taking this route.

Inside Guaranteed Acceptance Policies

Guaranteed acceptance burial insurance asks virtually zero questions and accepts almost all applicants regardless of health. The premium runs higher because the carrier takes on significantly more risk. To balance that financial risk, the policy mandates a two to three-year waiting period.

If you pass away from natural causes during that window, the beneficiary receives all paid premiums plus interest. According to industry data from Agent Pipeline, the interest rate is typically 10 percent depending on the specific carrier. Our customers appreciate that the full benefit automatically kicks in after the waiting period ends.

This setup ensures your family receives financial help when they need it.

How they map to the three plan tiers

These two structures determine if you receive level, graded, or guaranteed issue coverage. Simplified issue typically grants you access to the level or graded tiers, while a guaranteed issue final expense plan always maps to the guaranteed issue tier. We use this mapping system to match applicants with the fairest pricing. These structures map directly to the categories covered in our guide to level vs. graded vs. guaranteed issue.

| Feature | Simplified Issue (Level Tier) | Guaranteed Acceptance (Safety Net) |

|---|---|---|

| Health Questions | 8 to 15 yes or no questions | None (or minimal) |

| Coverage Start | Immediate (Day One) | 2 to 3 year waiting period |

| Value per Dollar | High (Lower premiums) | Lower (Higher premiums) |

| Target Applicant | Manageable health conditions | Severe or terminal conditions |

So in practice, the choice between simplified or guaranteed acceptance is really a question about your current health status. Do you qualify for level coverage, or do you need the safety net? Our priority is to find out if you qualify for the level tier first. Recent 2026 market data from PinnacleQuote shows that day-one level coverage provides two to five times more value per dollar compared to guaranteed issue plans.

When simplified issue is the right choice

Simplified issue is the right choice if you can answer “no” to questions about serious health conditions like active cancer or recent organ transplants. The premium per dollar of coverage is much lower, and the full death benefit is available immediately. We recommend trying for this specific tier first whenever possible. This process does not require an exam or lab work.

Common applicants who fit simplified issue include:

- Adults with controlled chronic conditions like high blood pressure, diabetes, or arthritis.

- Individuals with a heart attack or stroke history older than two years.

- Patients with cancer in remission for more than two years.

- People with mild to moderate COPD.

- Adults who feel relatively healthy and have not been hospitalized recently.

The Honesty Factor in Underwriting

Misrepresenting your health on a simplified issue application creates serious contestability problems in the first two years of the policy. MoneyGeek explains that carriers use third-party prescription databases and motor vehicle records to verify your answers instantly. If a claim is filed in that initial window and the carrier discovers a discrepancy, they can review or deny the payout completely. You must answer honestly. We always tell clients to take the guaranteed acceptance option if their honest answers require it, because that coverage is secure and real.

When guaranteed acceptance is the right choice

Guaranteed acceptance is the right choice if you have already been declined for a simplified issue policy. You should also apply for this safety net if you have a severe medical condition that triggers an automatic decline. We help clients secure this coverage when traditional underwriting is simply not an option. The mandatory waiting period feels like a long time, but the financial structure is actually quite fair.

Your premiums plus a standard 10 percent interest rate are completely refunded to your family if death occurs from natural causes during that window. You are never simply out of the money. Our experience shows that most applicants easily survive the waiting period. After that time passes, the full death benefit is securely in force just like any other life insurance policy.

In 2026, the National Funeral Directors Association reports that the median cost of a traditional funeral with a viewing and burial reached approximately $8,300 to $9,995. This high cost makes securing any form of coverage essential for protecting your loved ones. For a deeper look at how that timeframe actually works in practice, see our detailed guide on how the waiting period works.

Key Triggers for Guaranteed Acceptance

You should bypass the simplified application and go straight to guaranteed acceptance if you face specific health challenges. These common triggers include:

- An active cancer diagnosis or currently receiving treatments.

- A recent organ transplant within the last 24 months.

- A diagnosis of dementia or Alzheimer’s disease.

- An advanced respiratory condition requiring supplemental oxygen.

- A terminal illness with a life expectancy of less than 12 months.

The simple decision path

Finding your best policy requires a logical, step-by-step approach starting with the most affordable option. You should always attempt to qualify for simplified issue coverage before accepting a guaranteed policy. We guide our clients through this exact sequence every single day. Follow these simple steps:

- Try simplified issue first. Allow the carrier to check your medical background to see if you qualify for day-one coverage.

- Apply for guaranteed acceptance if declined. Use this as your reliable backup plan to ensure your family has financial protection.

- Pick a realistic face amount. The national median cost for a traditional funeral in 2026 is around $10,000, so a $10,000 to $15,000 policy is a smart starting point.

- Confirm your beneficiary designation. Keep this information updated so the funds go exactly where you intend them to go.

The Funeral Advantage product covers both of these underwriting structures. Call (800) 930-7459 to find out which specific tier you qualify for today. We have a team of licensed advisors ready to help. An expert will walk through the questions with you in real time and provide an answer the very same day.

Frequently Asked Questions

Are they two different products?

Which is cheaper?

Should I always try simplified issue first?

Learn more about Guaranteed Acceptance Burial Insurance

Whole life burial coverage with no medical exam and easy qualification, built for seniors with health concerns or prior denials.

Explore Guaranteed AcceptanceRelated Guides

Burial Insurance After Being Denied Life Insurance

Been declined for life insurance? Guaranteed acceptance burial insurance is built for you — no exam, pre-existing conditions accepted, here's what changes.

Burial Insurance With No Medical Exam, Explained

No-medical-exam burial insurance uses a one-page application. Learn how simplified-issue works, the health questions, and who qualifies same-day.

Can You Get Burial Insurance With Pre-Existing Conditions?

Yes — most applicants with pre-existing conditions can get burial insurance. Which conditions are accepted, the health questions, and the no-exam process.

How the Modified Benefit Waiting Period Works

Understand the 2–3 year modified benefit waiting period, the premium-plus-interest refund if death occurs during it, and when full benefits begin.