comparison

Preneed Funeral Contract vs. Final Expense Insurance

Preneed locks prices with one funeral home; final expense pays flexible cash to your family. Compare cost, control, and who each option suits best.

Updated June 25, 2026 · 7 min read

The basic structural difference

We know from experience that the toughest part of planning ahead is choosing between the rigid certainty of a contract and the flexibility of cash. A preneed funeral contract is an agreement with a specific funeral home where you prepay for designated services. In contrast, final expense insurance is a small whole life policy that pays a cash benefit directly to your family.

We founded Nationwide Final Expense on a simple mission to provide exceptional final expense life insurance services that customers can truly rely upon. This guide translates the high-level comparison from our parent page about Preneed vs. Final Expense Funding into a practical set of choices.

Understanding the difference between preneed vs final expense insurance matters more than ever.

Data from the National Funeral Directors Association highlights exactly why this choice carries so much weight. We see average costs for a traditional burial with a vault reaching $9,995 in 2026. That sharp price tag makes it critical to select the right funding vehicle before the need arises.

Let us review exactly what each option locks in, examine the latest financial data, and outline how to select the right strategy for your household. You generally have two primary paths to secure those funds:

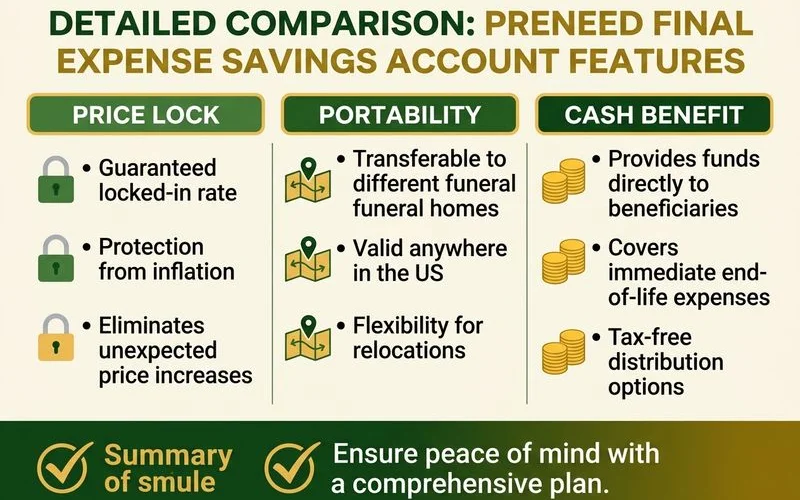

- Preneed Contracts: You prepay for specific services, and the home commits to providing them later at the agreed price. Texas law actually mandates that a trust or insurance policy holds your funds safely, keeping them completely out of the facility’s operating account.

- Final Expense Insurance: You pay fixed monthly premiums for a set cash benefit. When you pass, the unrestricted cash goes to your beneficiary to cover the funeral, travel costs, or remaining bills.

Side-by-side on the key dimensions

The core difference lies in flexibility versus locked-in guarantees. You commit to either one specific funeral home or a licensed insurance carrier, which in our case is the Funeral Advantage carrier.

Our clients often ask how these choices hold up against inflation and life changes. Evaluating a funeral contract vs insurance reveals a stark contrast in family control. We created this comparison to help you weigh the specific trade-offs side by side.

| Comparison Factor | Preneed Funeral Contract | Final Expense Insurance |

|---|---|---|

| Who you commit to | One specific local funeral home. | A licensed insurance carrier; family chooses the home later. |

| What is locked in | Today’s exact price for specific items listed in the contract. | A fixed cash face amount and a fixed monthly premium. |

| Inflation exposure | Specified items are protected. Anything not in the contract is fully exposed to price hikes. | The face amount does not grow with inflation, but your premium also never increases. |

| Portability if you move | Severely limited. Transfers usually trigger high fees and partial refunds. | Fully portable. The cash travels to your family anywhere in the US. |

| Non-funeral costs | Typically zero coverage for outside debts or final medical bills. | The full benefit provides unrestricted cash for any need. |

| Family flexibility | Survivors are locked into the exact services you pre-selected. | Your family retains full control to decide what services make sense. |

| Service quality control | Pre-agreed with one facility, regardless of future management changes. | Family selects the best home at the time of need, often utilizing FCGS price-shopping. |

We highly recommend reviewing what is a preneed funeral contract to grasp the strict structural boundaries of these agreements. Understanding those limits prevents unwelcome surprises for your loved ones down the road.

The 20-year question

A preneed contract bought today for an Austin funeral home might be redeemed in 5 years or in 25 years. The longer the gap, the more risk on portability (you might move, the home might change owners), and the more value from the price lock on specified items. Family situations rarely stay static over 20 years.

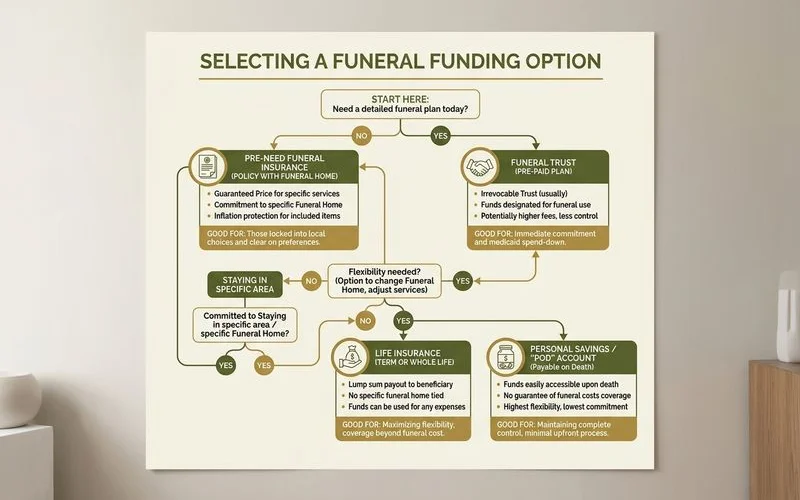

When preneed is the better choice

A preneed contract makes the most sense if you have deep ties to one specific facility and no intention of relocating. This strict commitment locks in today’s rates for specific services.

Our team respects that some folks prefer a heavily structured plan that leaves zero decisions for their survivors. It works beautifully for very specific, static circumstances.

Staying Local and Committed

You derive massive value from a preneed price lock if you plan to stay in your current city long-term. Portability concerns vanish entirely when your roots are permanently planted.

We see this frequently with families who have used the exact same Austin-area funeral home for generations. Signing a contract ensures you receive the same local care without worrying about future price hikes.

Complete Decision Removal

Some individuals want every single detail planned and paid for in advance. Preneed remains the most definitive way to achieve a zero-stress scenario for your grieving survivors.

Our experience shows that removing the burden of choice is a profound gift to a grieving spouse. The funeral home simply executes the predetermined contract.

External Costs Are Already Handled

You must consider what happens beyond the basic funeral service itself. A preneed contract is ideal if you already possess a strong financial reserve for everything else.

Recent studies from the National Bureau of Economic Research show that average out-of-pocket medical costs for seniors at the end of life often hit $11,618. We advise choosing preneed only if your savings, existing life insurance, or other assets can comfortably absorb those heavy medical bills, transportation fees, and headstone costs.

When final expense is the better choice

Final expense insurance provides the best solution if your family needs flexibility or if you might relocate in the future. Cash adapts to any changing circumstance your survivors might face.

Our advisors strongly favor this route for seniors wanting to cover both the funeral and lingering medical or credit card debts. The simple administration creates a very clean safety net.

High Portability and Family Flexibility

Cash benefits travel with you freely across state lines. A preneed contract simply does not offer this freedom.

We looked at a 2024 retirement study indicating that over 250,000 Americans relocated for retirement in a single year. You need a portable plan because moving to be closer to family or medical specialists is highly common.

Adapting to Modern Preferences

Your family might decide that a different service style makes more sense when the time actually comes. Final expense cash adapts effortlessly if survivors prefer a simple cremation instead of a lavish burial.

Our policies ensure the family holds the purchasing power. Comparing a prepaid funeral vs life insurance highlights how cash gives your family the ultimate final say.

Support for Price-Shopping

A Funeral Advantage policy completely changes how your family interacts with local homes. It includes dedicated Funeral Planning Assistance to help survivors during the worst days of their lives.

We proudly offer access to a Personal Funeral Advisor who steps in immediately. This expert compares prices at up to three local homes on the family’s behalf, ensuring your hard-earned cash goes further.

The combined approach

Many Central Texas families successfully utilize both options to secure their final arrangements. A small preneed contract handles the service itself at a specific home, while a final expense policy covers everything else.

We often see this hybrid strategy provide deep peace of mind. The contract delivers a strict price lock on merchandise, while the insurance policy provides necessary cash flexibility.

Combining the two methods protects your family across multiple fronts:

- Merchandise Protection: You beat inflation on specific items like the casket and vault.

- Ancillary Expenses: Your family has immediate cash for travel, medical debts, or reception costs.

- Legacy Building: Any remaining cash benefit serves as a small inheritance for your loved ones.

Our team is ready to help you evaluate which structure fits your specific household budget. Because we do not sell preneed contracts, this cost comparison remains completely objective.

If you want to talk through these burial insurance vs preneed strategies, call (800) 930-7459. The conversation is totally free and takes about 15 minutes.

Frequently Asked Questions

Which option pays out faster?

Which costs less long-term?

Can I have both?

Learn more about Preneed vs. Final Expense Funding

Plain-English help deciding between locking in prices with a funeral home and keeping flexible cash with final expense insurance.

Explore Preneed vs. Final ExpenseRelated Guides

Pros and Cons of Prepaying an Austin Funeral Home

Prepaying a funeral home has real upsides and real risks: portability, refunds, what happens if the home closes or you move. See both sides honestly.

What Is a Preneed Funeral Contract?

A preneed funeral contract lets you prepay and lock in prices with a funeral home. How it works in Texas, what's locked in, and the oversight that protects you.