definition

What Is Final Expense Insurance and How Does It Work?

A plain-English guide to final expense insurance: what it is, how it works, who it fits, and why premiums never rise.

Updated June 25, 2026 · 6 min read

`

We talk to families every day who are caught off guard by the rising costs of end-of-life care.

Nationwide Final Expense was founded with a simple mission: to provide exceptional final expense life insurance services that customers can truly rely on when facing these difficult transitions.

The reality is that sudden expenses cause immense stress for grieving relatives, making it vital to understand what is final expense insurance and how it provides a clear path forward. Let’s look at the current data to see what it actually tells us about funeral pricing, and how a dedicated policy protects your hard-earned savings.

A simple definition: What is final expense insurance

Final expense insurance is a small, permanent whole life policy designed specifically to pay for your funeral and burial costs. Most of these policies offer a face amount between $5,000 and $35,000 to match typical end-of-life expenses.

You pay a fixed monthly premium for the life of the policy, and when you pass, the death benefit is paid in cash to the person you name. This immediate cash on hand makes a difficult time much easier for your loved ones.

Current US Funeral Costs

Our research into the 2026 National Funeral Directors Association data shows the median cost of a traditional funeral is approximately $8,300. Adding a standard vault pushes that price tag closer to $10,000, leaving many seniors searching for a reliable safety net.

- The Social Security Gap: The US government death benefit pays a flat $255.

- Inflation Impact: That payment amount has remained completely unchanged since 1954.

- The Solution: Small whole life policies bridge the gap between government help and actual costs.

This specific product ensures your family avoids going into debt to pay the local funeral home. For Central Texas seniors who have looked at guaranteed acceptance coverage, understanding the core policy is the best place to start.

We should note that the technical name for this product is small whole life insurance. The phrase “final expense” is simply descriptive, as it tells you exactly what the coverage is for, and the two terms are used interchangeably across the industry.

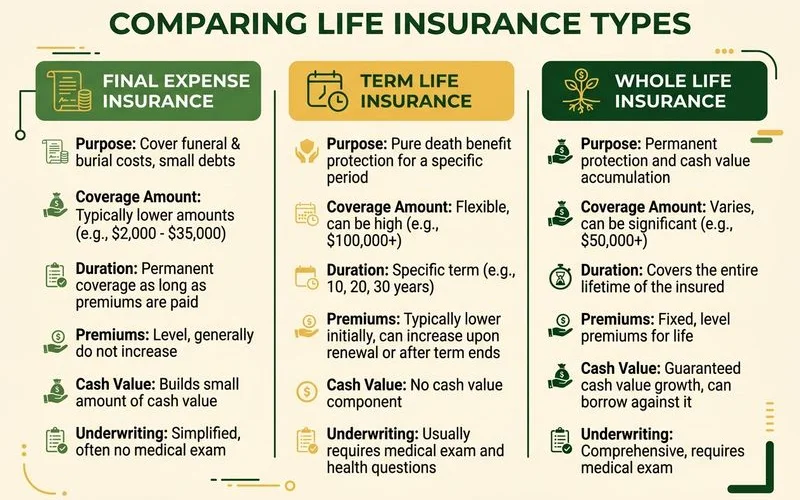

How it differs from term and standard whole life

Term life insurance covers a fixed period, usually 10, 20, or 30 years, and if you outlive the term limit, the protection simply ends. We frequently speak with clients whose term policies expired right when they needed them most, typically around age 80.

Standard whole life insurance offers hundreds of thousands of dollars in coverage, but it requires a full medical exam. These large plans are priced accordingly and can be difficult for retirees to afford on a fixed income.

| Feature | Term Life | Standard Whole Life | Final Expense |

|---|---|---|---|

| Coverage Length | 10 to 30 Years | Lifelong | Lifelong |

| Face Amount | $100,000+ | $250,000+ | $5,000 to $35,000 |

| Medical Exam | Often Required | Always Required | Never Required |

The Simplified Underwriting Advantage

Our advisors find that seeing final expense insurance explained clearly proves it is the perfect middle ground. It provides lifelong protection as long as premiums are paid, and the underwriting process uses a simplified-issue model.

This approach means there is absolutely no medical exam required to get approved. Clients appreciate how quickly the process moves from application to final coverage.

- Fast Applications: Qualification is based on a one-page application with a few health questions.

- Database Checks: Carriers verify your answers using prescription databases like Milliman IntelliScript.

- High Approval Rates: Most applicants qualify easily, including many with pre-existing conditions.

We love sharing the best feature of this coverage with new policyholders. The stability of the pricing structure brings immense peace of mind.

One bottom line

Premiums are level. The rate you start at on day one is the rate you pay for the life of the policy. It cannot be raised because you age or your health changes.

What’s covered, what’s not

The death benefit is paid in unrestricted cash directly to your named beneficiary, meaning that money can be used for the funeral, cremation, memorial services, or a headstone. This flexibility ensures your family can respond to unexpected costs as they arise.

We want to emphasize that there is no requirement for the money to be spent at a particular funeral home. Families use these funds for a wide variety of urgent expenses, giving your beneficiary total control over the financial decisions.

Common Covered Expenses

Beneficiaries often rely on the cash for specific end-of-life needs that go beyond the burial itself. The payout can be directed toward several immediate priorities.

- Basic Service Fees: Covering the standard funeral home overhead, which averages $2,495.

- Caskets and Urns: Paying for a metal burial casket or an alternative cremation container.

- Outstanding Debts: Settling remaining medical bills, transportation costs, or probate attorney fees.

Understanding the Fine Print

We always explain the legal limitations upfront to avoid any surprises for your family. What is not covered is contractual fine print regarding application accuracy, as final expense policies typically have a contestability period during the first two years.

- The Two-Year Rule: If the cause of death is misrepresented on the application, the claim can be reviewed.

- Accurate Disclosure: Honesty about your health history is critical to ensure a guaranteed payout.

- Full Protection: After 24 months, the coverage is fully in force exactly as written.

Who it fits

Final expense insurance fits people aged 50 to 85 on fixed incomes who want to protect their families. This product ensures your children are not left with a massive bill for end-of-life expenses.

Our agents see how a sudden medical event can easily wipe out a modest retirement account. It is especially useful for adults who have been declined for standard life insurance because of age or health.

Designed for Health Challenges

Simplified-issue and guaranteed-issue versions are built for exactly that situation. These specialized options provide coverage when traditional paths are closed.

We help clients find specific policies from carriers that accept severe medical backgrounds. This targeted approach offers several distinct advantages.

- Guaranteed Acceptance: Certain policies cannot decline you for health reasons.

- No Medical Exams: You never have to meet with a nurse or provide a blood sample.

- Fixed Budgets: The premiums remain locked in for life, making monthly planning simple.

Sizing the Policy Correctly

It is not a substitute for income replacement, so if you have a young family and need to replace decades of income, a much larger term policy is the right tool. We use a burial insurance definition that focuses strictly on the predictable cost of dying.

Whole life final expense ensures your loved ones are not burdened by these bills. The policy size should be matched directly to your local prices.

| Service Type in Austin Area | Estimated Cost |

|---|---|

| Traditional Burial | $7,912 |

| Cremation with Service | $5,890 |

For example, the Cremation Association of North America projects that over 63 percent of Americans will choose cremation by 2026, which lowers the required coverage amount. Adjusting your face amount based on these choices keeps your premiums affordable.

Conclusion: Securing Your Final Arrangements

We can help you see whether this is the right fit for your specific situation, and a licensed advisor can walk through the numbers with you in about 10 minutes. The quote is completely free, with no medical exam and zero pressure to buy. If you are still weighing the decision, our honest look at whether final expense insurance is worth it for seniors lays out both sides.

Most callers learn within a few minutes which exact plan applies to them. Our system makes it easy to start by requesting a free quote online to secure your legacy.

Frequently Asked Questions

How much does final expense insurance cost?

Does final expense insurance build cash value?

Who should buy final expense insurance?

Related Guides

How Much Does a Funeral Cost in Texas? (2026)

Real Central Texas funeral costs in 2026: traditional burial averages, cremation pricing, what drives cost, and how much coverage your family actually needs.

How the 24-Hour Claim Payout Works

A step-by-step look at how approved Funeral Advantage claims are paid within 24 hours, what starts the clock, and how families receive cash.

How to Pay for a Funeral With No Money

Practical ways to cover funeral costs when there's no money: county burial assistance, payment plans, crowdfunding, and how final expense insurance bridges the gap.

Is Final Expense Insurance Worth It for Seniors?

An honest look at whether final expense insurance is worth it for seniors — real funeral costs, fixed premiums, who benefits most, and when it isn't the right fit.